Qualstar is an American manufacturer of power supplies (N2Power) and back-up systems, in particular tape libraries. While this technology may seem somewhat outdated, tapes offer low-cost data storage, and provide an offline alternative to cloud storage. The company employs around 15 people and is not particularly capital-intensive.

Alright, let’s start with the numbers.

Market Cap = $ 4.500.000

Shares out = 1.925.025 (1.090.366 in public float or about 50%)

Cash = $ 4.700.000

Debt = No significant loans or long term debt

Taking the long-term liabilities into account, my estimation for the enterprise value is around $ 1.000.000.

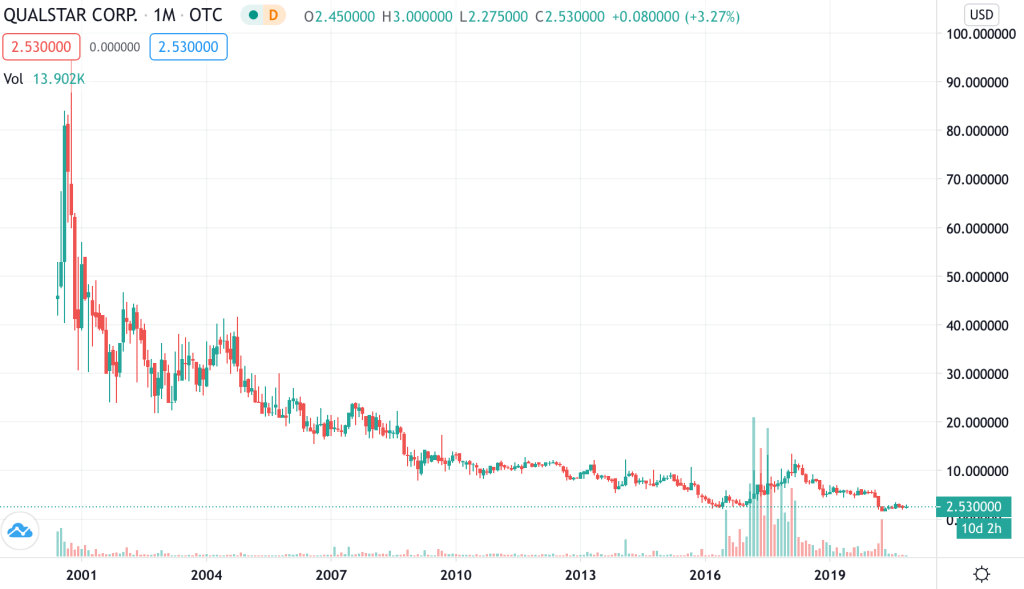

The company has been around for a while, the IPO took place in 2000 amidst the height of the dot com bubble. Basically, the price is been going downhill from that point. While the stock is bottomming out, one cannot spot a reliable base, yet. The price action is still somewhat bouncy, with volume on the high side.

The CEO owns in excess of 40% of the shares, and he purchased some in 2019 for a price about double today’s price. Of course, this was pre-pandemic.

So, is the company making any money? Well, yes, at times. Revenue has been growing over the past years and after many years of losses, the company has reported some profits. Also, they have been buying back some stock. The revenues between storage and power supply are distributed around a 60/40 basis, currently. The storage business is significantly more profitable than the power supply business, whose revenues have been declining.

| Year | Revenue | Net income | Equity | # Shares out |

| 2015 | $ 12.902.000 | $ -1.308.000 | $ 7.910.000 | 12.253.000 |

| 2016 | $ 9.417.000 | $ -1.210.000 | $ 4.839.000 | (1/6 split) 2.042.019 |

| 2017 | $ 10.641.000 | $ 640.000 | $ 5.896.000 | 2.042.019 |

| 2018 | $ 12.229.000 | $ 1.468.000 | $ 7.328.000 | 2.030.017 |

| 2019 | $ 13.439.000 | $ -7.000 | $ 6.743.000 | 1.925.025 |

The year 2020 will probably not be a good one, with the Covid pandemic as a major factor. Orders have been delayed and global supply has been disrupted.

To summarise, I like the business. The business model is fairly simple, so are the products, with nothing really sexy or exciting about them. I think demand for these products will remain. Given the strong balance sheet, I think the company can remain for quite a long time, even with earnings being negative for most of the years. I’m holding a small position at this moment. The company filed a 15-12 and is going dark, which might cause the price to drift lower. I will probably add to my position in the time to come.

Regards,

Thijs

Disclaimer: Long QBAK