Every now and then, whilst scanning through the OTC Markets, I come across companies with very low market caps, between 100 and 200k. Usually, these are empty shells and merely remnants of the past. Rarely, a company is still in business. Even more rarely, the company is making money. Alliance Creative Group is such a business. As I was writing this post, I found myself checking numerous times if the market cap was indeed six figures. Sit tight, as this is an odd one.

The company is in the business of retail packaging and fulfilment. It leases space in 8 warehouses throughout the United States, which are used as packaging and distribution points for order fulfilment. They started a trucking business in 2016, but transitioned it to another company in 2018. The company owns shares in a subsidiary called PeopleVine, which is a “Member Experience CRM that lets you create digital engagements and self-service tools for your members”.

Conveniently, the company has an up-to-date website with some information on it. They have not been too consistent with their reporting, but at least there is some material published in each of the past fiscal years.

Some numbers:

Market cap = $ 160.000

Common shares out = 1.073.044 (Free float is around 90%)

Note that there was a reverse split with a ratio of 4000:1 in August 2019. The common shares are not entitled to any dividends.

Preferred shares = 747.994. These are cumulative with a 4% stock dividend. Most of it is owned by the CEO.

Cash is low, and with current liabilities of $ 1.799.028, the company is simply not very solvent. Assets (not assests) like “Employee Advances” of $ 421.841 seem somewhat ridiculous in my opinion. The number has declined from last year however, so at least someone’s paying their advances back. Apart from the preferred stock there are convertible notes which have the potential to significantly dilute the equity.

Let’s just forget about the balance sheet for now and conclude that it’s unlikely for investors to receive one penny in the case of liquidation. Moving on. Below is a screenshot of the income statement.

The net income, earned in the past three months, exceeds the market cap of the entire company. Yes, the balance sheet is dubious. Yes, there are preferred shares, and a lot of them. Yes, share dilution will happen, and probably to a large extent. However, never before have I paid $ 0,15 for a share with quarter earnings being $ 0,16 per common share.

So, what about this subsidiary, PeopleVine Inc.? Last year, ACG invested a total of $ 720.000 in in this business (see note 5 of the financial statements, in the Q3 2020 report). There are other investors at the table, ACG owns 3.364.375 common shares which, according to them, have a value of $ 2.523.281. I’m really not sure how to assess this and it’s safe to say I’m sceptical. Additionally, since the product is partly used for physical events, business might be impaired this year.

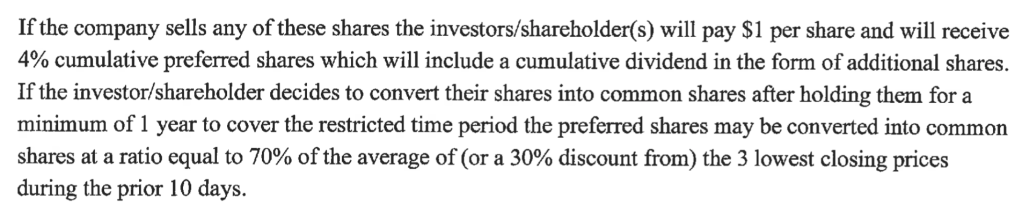

The share structure of ACG is complicated and I’m still trying to wrap my head around it. Regarding the series H preferred stock, the company states the following:

At this point I have to admit that it’s very difficult to assign a value to this business. On the one hand, shareholders of ACG are in a very weak position and may not reap any benefits, even if the company does relatively well. On the other hand, the company is real, it exists, money is made, and the share price is historically low. I still think the market cap is somewhat insane for a functioning business. I’m wondering what the catalyst for share price growth could possibly be. Perhaps simply survival of the fulfilment business will prove to be sufficient. Perhaps PeopleVine will prove to be a successful platform in the longer term. Who knows.

Based on the long range chart, I will take a position and just follow the company for the time to come.

Thank you for reading. Regards,

Thijs

Disclaimer: Long ACGX

I love interesting, under the radar blogs like these. I find this write-up intriguing.

1) Regarding price appreciation: it appears this company is profitable. How reliable is the financial information they’ve shared so far? quarterly earnings equal to the market cap is rediculous and if accurate, this company will simply become a pile of cash (if they don’t di-worsify). If accurate, a dividend or payouts are a matter of time.

2) Price chart: why has price dropped 100 fold in the past ~5 years?

I look forward tp hearing from you.

LikeLike

Hi Maithem, thank you for taking the time to read my blog.

Tiny companies like this one come with substantial risks, I would always be careful when assessing the financials and I wouldn’t trust them a 100%. Also, the fulfillment business did well during the Covid lockdowns of the past year, it’s unclear weather this tailwind will persist.

Regarding your second point, I guess the share price went close to zero at some point. The company did a 1/4000 reverse split, probably to get some meat back in to the share price. This way, in the long range price chart, historic prices are blown up to high levels. I’m not sure but this is my best guess.

Regards, Thijs

LikeLike